Improving your personal finances is a necessity regardless of your income level. When it comes to personal finances, it is always good to establish better habits but some may not know what steps to take to better manage their finances. Toward that end, here are five things you can do to make an immediate and lasting positive impact on your finances this year.

Set Up an Emergency Fund: Before we can make headway in other areas of our financial lives, it is important to have a plan in place for emergencies. We all know that unexpected expenses happen, and if we have no money in place to deal with these situations, we will end up taking it from other places. Many advisors say it is best to start with something small and attainable, such as $1000. Put away this sum of money as quickly as possible. Next, continue regularly adding to the fund until you have 6 to 12 months of income saved.

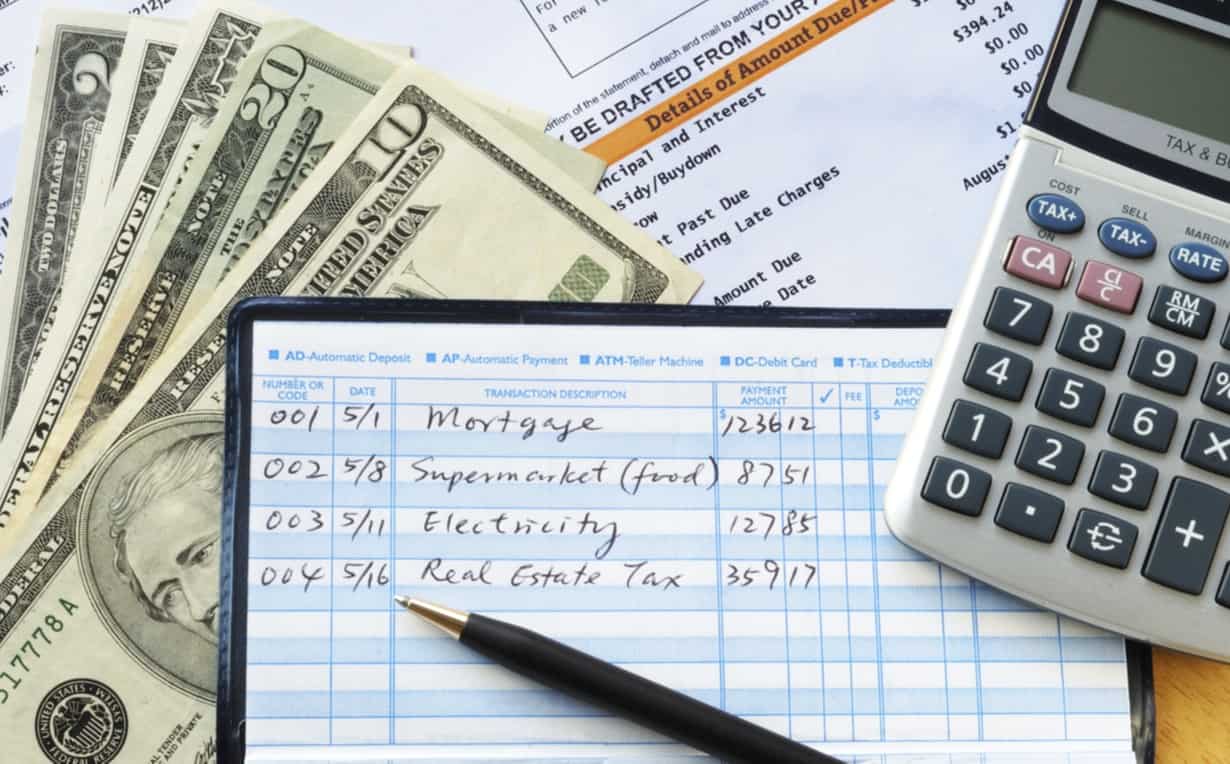

Establish a Budget and Stick to It: Many people do not like the idea of a budget because they believe it puts too many restrictions on their financial behavior. Actually the opposite is true. What a budget does is give you an organized financial picture; income, fixed expenses, savings, discretionary spending, etc. Once you know you have the proper amount going to each category, you gain more freedom to spend money on fun things without feeling guilty.

Implement a Debt Reduction Plan: The average American has somewhere in the neighborhood of $10,000 in credit card debt. If you are pretty close to average in this area and you are only making the monthly minimum payments, the debt is far more likely to increase than decrease if you are not proactive. The best strategy is to designate a certain dollar amount (that you can afford) each month and use it to pay down your credit cards. This amount should be above and beyond your monthly minimums. Start with the card with the smallest balance and work your way up until they are all paid off. And of course, structure your budget so you do not end up using these cards for new purchases.

Save Wisely: Saving for the future is very important because you do not want to enter your retirement years living only on Social Security. Clearly, the best way to save for retirement is through a 401K or similar plan at work. You are able to contribute pre-tax dollars to the plan and in most cases the employer matches 25% or more of your contribution up to a certain percentage of your income. This provides a double benefit because it reduces your tax liability (you pay tax later when you withdraw from the plan at retirement) and you receive what amounts to free money from your employer in the process.

Start a Home Business: This may not be for everybody, but many people can benefit from starting a sideline business out of the home. These days, there are numerous ways to earn money from home. As always, do your due diligence to ensure that the business idea is legitimate. Having a home business not only provides the potential for an additional income stream, there are also numerous tax deductions you can take advantage of even if you fail to turn a profit the first few years. Speak to your local accountant to find out if this option might be right for you.